GroovyBank Puts $$$ in Customer Pockets: Cash Reward for Data Trade Powered by TIKI!

GroovyBank Puts $$$ in Customer Pockets: Cash Reward for Data Trade Powered by TIKI!

Legacy banks sell data and keep the profit! Groovy gives it back to their users. Far out, man!

Banks! Financial Institutions! Hooray!

81% of adults in the United States are “fully banked,” meaning they have a bank account and do not use other financial services such as money orders, check cashing services, pawn shop loans, etc. In short, being fully banked means you’ve got a bank account and that fits your financial needs. The number of fully banked Americans as reported in 2021 was up a full 10 percentage points from 2015. Everyone is getting banked up! It’s a party and pretty much everyone is invited! Like, 209 million people! Hope y’all remembered to bring the hors d'oeuvres!

The Problem:

If you’re a new or alternative bank trying to break into the industry, banking is one of the most difficult industries to conquer when considering competition. Why? Well, I just told you.

81% of their potential customer-base is already a customer somewhere else.

Fortunately, if you’re a bank or financial service paying attention to trends, then there are a few things worth noting that may be a boon to your upcoming success. First, keep in mind, people have a lifespan. I hate to be the bearer of bad news, but you’re going to die one day. And so are all of the other 209 million American adults that are currently banking. Established legacy banks continually need to attract new customers. For banks, folks under 40 who have a high level of education and income growth potential are a prime customer segment to target. This is the segment of the population that is considered “young.” Dang, banks are super old, man, but hey! I’m young!

But customer satisfaction scores for us youngsters (if you’re over 40 reading this, sorry dawg. What was Christmas like in the 80s?) has been steadily declining when it comes to legacy banks. For the nation’s largest banks, customer satisfaction was down 4 points in 2022 on a 1000 point scale from 2021, and 9 points from 2020. I don’t know much about 1000 point customer satisfaction scales, but JD Power tells me that this decline is “steep,” and that the very young and hip under-40 population is leading the charge. Among the complaints from the youths are the quality of branch service, new customer onboarding (probably a pretty important one), and resolving customer complaints. Uh-oh.

Additionally, intent to re-use the brand and perception of having a relationship with the brand are also in decline.

In layman terms, more and more Americans want out from their banks, and the customer experience is a major factor as to why.

Enter GroovyBank

Far-out man! Independent of year (and maybe worthwhile placing yourself in the shoes of a Woodstock attendee for this exercise), how many people do you think have ever referred to their banks as “groovy”? Probably not many. Banks are useful and necessary and 81% of people are fully banked up, baby! But despite what the commercials on cable TV try to convey, legacy banks, and banks in general, aren’t really viewed as being “cool” or “hip.” All the cool and hip 39-year-olds are bailing, remember?

Well, not anymore! GroovyBank is a new, up-and-coming digital bank, meaning, the banks’ services are delivered over the internet (a series of tubes). Now, customers are legitimately forced to claim their bank to be Groovy! Smart!

Anydangway, Groovy are sharp folks. Their go-to-market strategy has been centered around analyzing all of the things people don’t like about their current bank, and trying to do the opposite. The customer experience is a major point of emphasis for Groovy, and rightfully so. High or hidden fees, difficulty opening a new account, lacking or ineffective customer service, and having to wait, like, 3 days to access your direct deposit money from your shift at Dunkin’ even though banks have like, so much money, are among the common complaints regarding the customer experience held by consumers.

So Groovy is doing the opposite. No credit check required to open an account, no required minimum balance, no monthly or overdraft fees, tons of free ATMs across the country, high APYs, and a sleek and easy-to-use app are all promises made by Groovy to their current and potential customers.

Why these? Let’s ask Forbes!

Another thing on their side? By being digital-first, Groovy is satisfying a growing desire among Americans.

Going Digital

Digital banking is on the rise based on the needs and desires of the consumer. Close to 60% of consumers say they are interested in using a digital bank. For those who already do, 88% say they are satisfied with their bank’s services, compared to 66% using traditional, legacy banks.

In terms of demographics, 79% of millennials are interested in digital banking, compared to 34% of boomers. Very convenient! The olds aren’t interested by the youthful sub 40s of the world are looking to groove, which is perfect, and makes a ton of sense. After all, they are the demographic leading the steep decline in customer satisfaction at legacy institutions.

Alright sounds good, so what’s the problem. Well, being interested in something isn’t the same as using something, and an 88% percent satisfaction rate would be a whole lot sweeter if those interested folks became customers.

However, only 27% of Americans are currently using a digital bank.

I know what you’re thinking, 27%? That’s a sizable chunk of the market. And yes, you would be correct.

However, Groovy is very new. Outside of the top established digital banks, awareness of alternative digital banks among Americans is low. On top of this, legacy banks aren’t dumb. They are changing with the times. 60% of people are interested in digital banks, but 27% of people actually use them. 78% of people bank digitally, meaning most people who are digitally banking are doing so at a legacy bank. Legacy banks are constantly improving their apps and digital services to meet demand, and with enormous budgets and resources, they can do it quite well.

GroovyBank needs a competitive differentiator. They need something, some feature, some campaign to help set them apart, to get them recognized in the digital banking community and steal away customers from the legacy banks. And who do you turn to when you need a competitive differentiator?

You guessed it!

Enter TIKI

At this point, people are starting to recognize TIKI and the capabilities of our zero-party data licensing technology. GroovyBank came to TIKI with an idea in mind. They just needed a way to make it happen. They wanted not only to become a significant player in the digital banking sector, but also take a run at those legacy banks. And they believe they have the angle to make it happen: putting legacy banks on blast for selling their customers data (usually without them knowing) and pocketing all of the returns. Groovy then plans offering customers the option for a new revenue stream by trading their data for 100% of the sales when re-sold on secondary markets.

Before we dive into the solution, let’s get a quick breakdown on the history and pros and cons of “open banking,” as well as some insights into what banks are doing behind the scenes with customer data.

Open Banking

Open banking is the practice of allowing customers to share their financial data with third-party service providers via open APIs provided by banks. Basically, other companies and applications can access things like banking, transaction, and other data for a variety of reasons. Fintech companies have a lower barrier of entry, as accessing this information can allow for them to build new products and services to improve the customer experience with the exact, relevant information provided by banks and institutions.

Banks can implement services provided by these fintech companies into their customer experience. Over time, the networking of accounts and data across institutions can lead to a more complete understanding of consumers, allowing for more personalized and customized experiences.

This is helpful, as 44% of US bankers want a more personalized experience, while 51% of banks claim keeping up with customer needs that are constantly changing and in flux is difficult.

The Dark Side

While open banking can open up many avenues of opportunity, giving access to consumer data also brings about quite a bit of shady behavior, as you could imagine. Potentially the shadiest of the shady is the re-sale of bank transactional data. Yup, the records of what people buy, when and where they buy it, and how much they spend on it its corralled up, packaged together, and sold off to affiliate partners and data brokers.

Dang. That’s a lot of money.

Banks are selling consumer data and making profit? Surely this is illegal! Well, yes, and no. It would be illegal due to privacy initiatives such as GDPR and CCPA, but it becomes legal when, get this, a consumer agrees to let a bank sell their data.

If you’re a customer of a legacy bank such as Bank of America, Chase, Wells Fargo, etc, etc, then you more than likely have agreed to let them sell your bank and transactional data. Thanks, open banking!

Well, let’s not throw open banking under the bus, nor should we immediately jump to the conclusion that other companies having access to transactional data is a net negative. As mentioned, there’s a lot of positives that could come out of it: more personalization and access to more accurate discounts and offers, improved, more convenient features, and more. There are lots that can be accomplished with financial data as the fuel to the engine, and much of it can result in positive experiences for the consumer. The real issue is that most people are unaware that banks are selling their data.

The Solution:

Leveraging TIKI’s zero-party data licensing technology, let users willingly opt in to allowing GroovyBank to sell their data on secondary marketplaces, such as Snowflake, with the user receiving 100% of the earnings when the data is sold.

GroovyBank sells the data that the major legacy banks are selling, but instead of pocketing the money, Groovy passes back the rewards to their users.

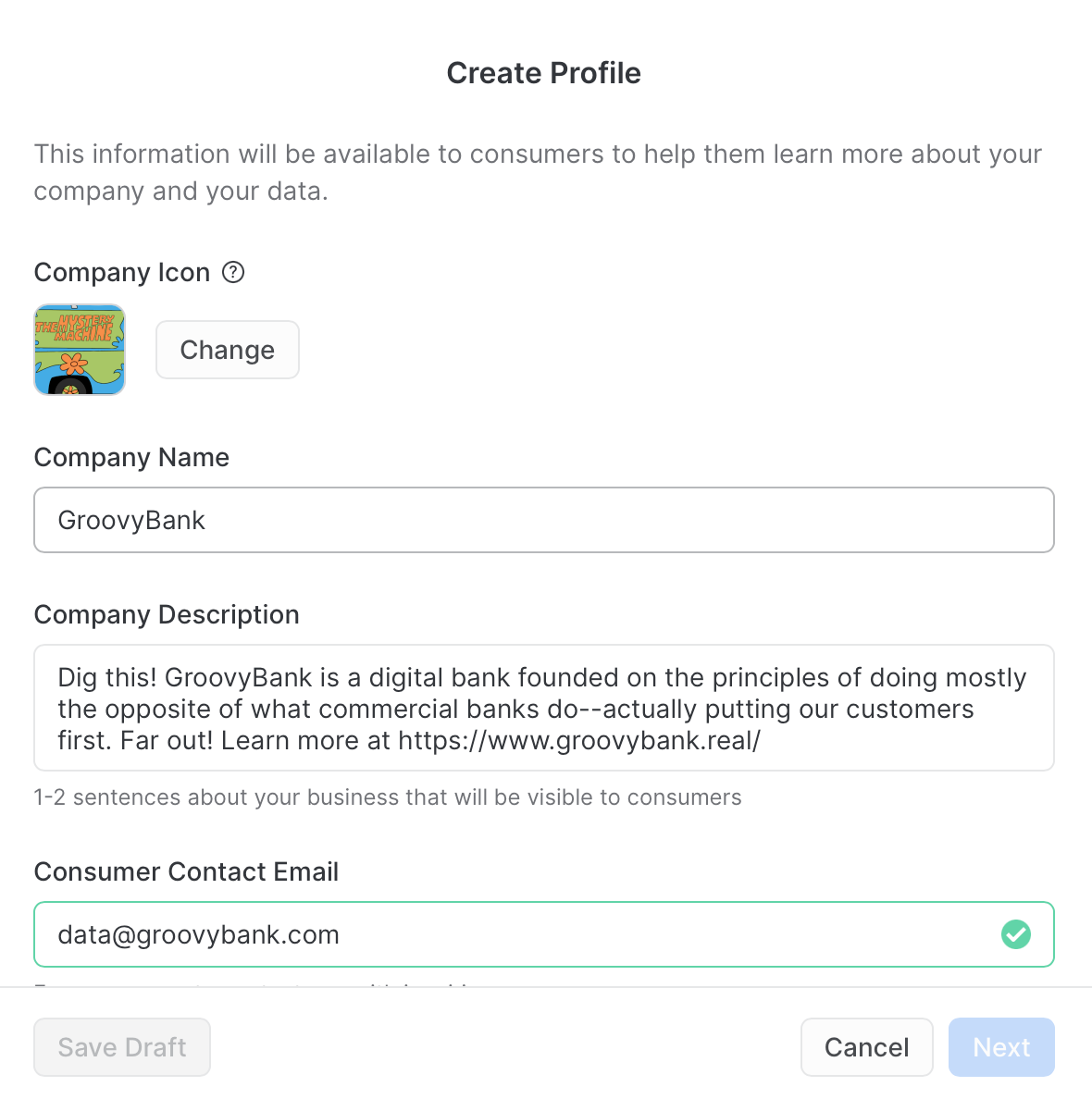

GroovyBank wants a competitive differentiator. They wanted a cool new feature to draw attention to their bank, and simultaneously they wanted to take a swipe at big banks. So TIKI built the cool new feature and let Groovy take all the swipes at legacy banks that their far out hearts could desire.

Here’s how it works:

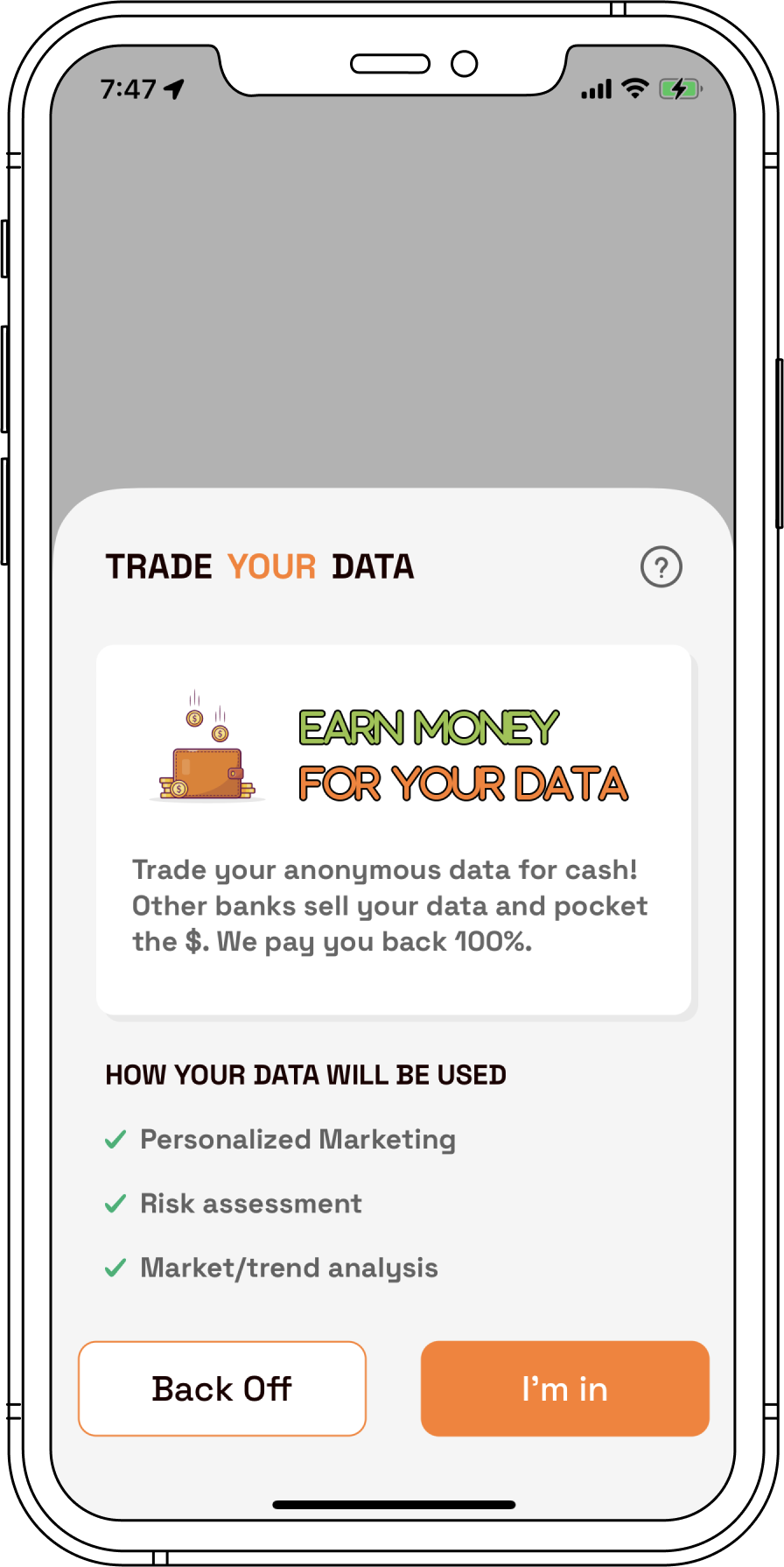

Utilizing TIKI’s technology, a data offer is presented to users within the GroovyBank app. The pop-up goes over the terms of a potential licensing agreement between the user and Groovy. As you can see below, the data offer is for trading anonymous financial data for 100% of the cash from the sale. It also shows how the data will be used, which in this case is personalized marketing, risk assessment, and market analysis. The image is just an example; the real offer would include details on the terms of the deal and clarification on its use cases.

If the user opts in, a contract is created and indexed by TIKI’s system. The wondrous powers of cryptographic hashing combine to generate an immutable (meaning it can never be altered) digital record of the agreement on the spot. It is an official record of consent and legally holds Groovy accountable for following the terms of the agreement. It also contains the record of what the user receives in return. Users can opt-out whenever they’d like. While the contract is binding, the user always has the option of changing their mind. They can even re-change their mind, and a brand-new contract is created in its place. Pretty nifty if we do say so ourselves.

After the contract is signed, there needs to be a way for Groovy to manage who agreed to what in terms of the data they can list. Groovy, like most fintech players, aggregate their data on Snowflake.

Using TIKI technology, customer datasets can easily be sorted between “consented” and “opted out” using a lambda function that takes in the pointer records from Snowflake’s dataset and, merges them with which records have consent for the specific program Groovy is running.

In essence, Groovy can add one line of code to their product, and for each program Groovy is trying to run, for example listing and re-selling data for the purposes of personalized marketing. All of this is powered by TIKI’s technology, from the creation of high-volume licenses, to the indexing, searching, sorting, and application of terms of service of each and every license.

From here, all it takes is Groovy filling out the standard Snowflake marketplace listing form, and they are on their way to monetizing data for their users. Totally cool! For a more detailed breakdown, here’s Mike showing off what we built.

Another win-win scenario. Groovy can run a marketing campaign taking shots at banks selling data without users knowing it, then offer a solution that puts cash back into the pockets of their users. Additionally, tons of cool programs and features can be built on top of the feature, for example, users could pool the earnings from data sales together to donate to charities and causes they believe in, or, if Groovy releases a premium feature in the future that costs money, users can pay for the feature by opting in to the data trade.

Of course, this is not just limited to banks and fintech players. Any business that wants to create additional revenue streams for their users could find this use case beneficial. Cash back for trading data is a hot idea, and actually the original idea TIKI was founded on. Now, it’s a powerful feature among many others!

If you’re interested in learning more, check out our website and book a chat with Mike. If you want more case studies, check them out below!